Why postponing corrections costs more than you think

Every organization deals with reporting mistakes. A misclassified expense here, a rounding error there, perhaps a data integration hiccup that creates duplicate entries. In isolation, these seem manageable. The temptation to defer correction is strong, especially when deadlines loom and resources are stretched. But this "fix-it-later" mentality creates a unique form of technical and organizational debt that accrues interest at a rate most leaders vastly underestimate.

Understanding the Compound Effect

Uncorrected reporting errors compound over time because each mistake becomes embedded in subsequent reports, year-over-year comparisons, trend analyses, and forecasting models. According to Gartner research, poor data quality costs organizations an average of $12.9 million per year (Gartner, 2023). A simple Q1 classification error influences strategic resource allocation decisions by Q4, meaning a $50,000 misattribution can ultimately affect millions of dollars in business decisions across the fiscal year as downstream analyses incorporate the flawed data. The SEC treats uncorrected misstatements cumulatively under SAB 99 and SAB 108, meaning even individually immaterial errors can become material in aggregate.

Unlike financial debt where interest rates are clearly stated, reporting debt compounds in less obvious but equally damaging ways. Each uncorrected mistake becomes a foundation upon which future reports, analyses, and business decisions are built. Consider what happens when a Q1 revenue figure contains a classification error that goes uncorrected.

By Q2, that error has been incorporated into year-over-year comparisons. By Q3, it's affecting trend analyses and forecasting models. By Q4, strategic decisions about resource allocation have been made based on flawed data. The original error, perhaps a simple misattribution of $50,000 in revenue, has now influenced millions of dollars in business decisions.

The Hidden Interest Rates

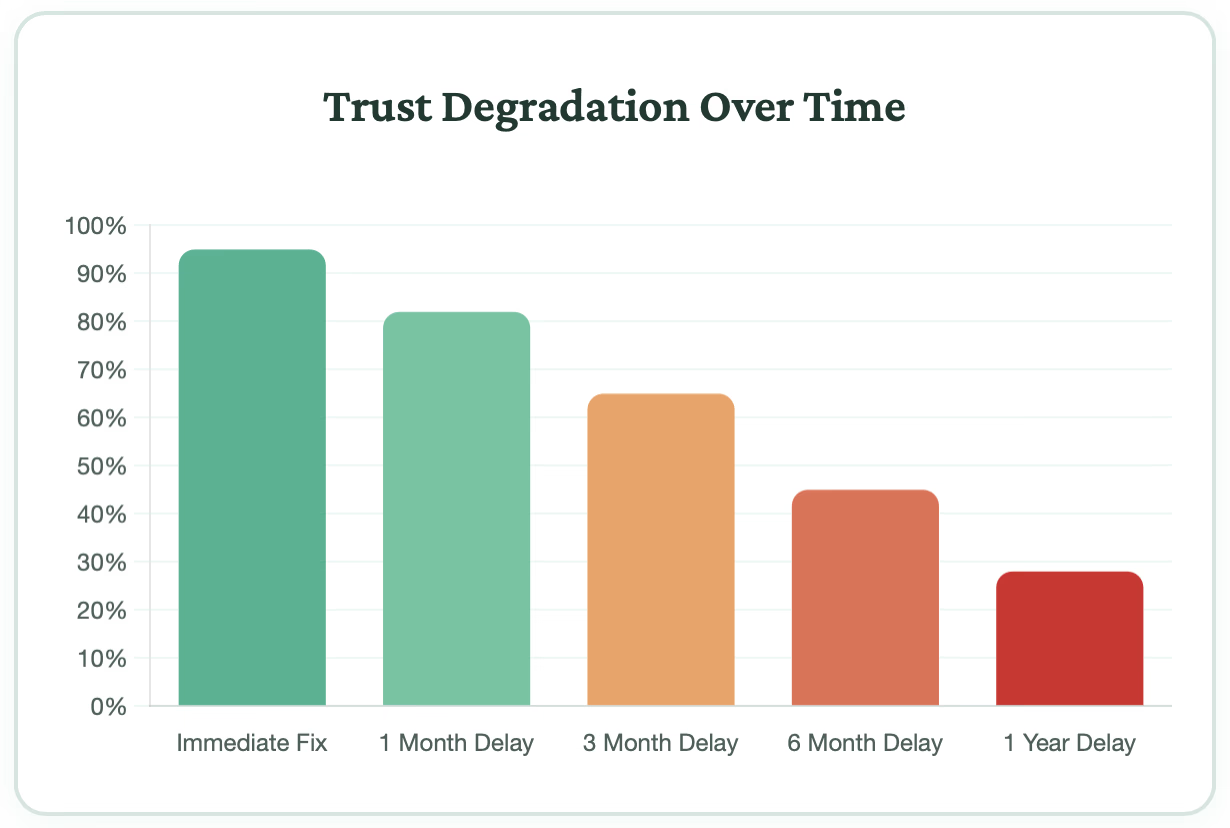

Uncorrected reporting mistakes accrue three forms of hidden interest: operational complexity interest as teams develop workarounds and manual adjustments, decision quality degradation as executives allocate budgets and resources based on flawed data, and trust erosion tax as stakeholders lose confidence in reports and resort to gut instinct or shadow spreadsheets. SEC Chief Accountant Paul Munter has stated that "the accumulation of uncorrected misstatements is an area of continued focus for the SEC staff, as individually small errors can aggregate to levels that materially mislead investors" (SEC Office of the Chief Accountant, 2023). The trust erosion rate is typically the most damaging because it undermines the entire reporting infrastructure.

To truly understand the cost of uncorrected reporting mistakes, we need to examine the various "interest rates" that accumulate over time. These aren't measured in percentages, but in concrete business impacts.

1. Operational Complexity Interest

Every uncorrected error adds a layer of complexity to your reporting infrastructure. Analysts must remember which reports contain which errors. Finance teams develop workarounds and manual adjustments. New employees inherit undocumented institutional knowledge about "the numbers we don't trust." This operational overhead compounds monthly, eating into productivity and increasing the likelihood of new errors.

2. Decision Quality Degradation

Perhaps the most insidious form of interest is the degradation of decision quality. When executives make strategic choices based on flawed data, the consequences ripple throughout the organization. Marketing budgets get allocated to underperforming channels. Product development resources flow to initiatives that appear more promising than they are. Hiring decisions get made based on growth trajectories that don't exist.

3. Trust Erosion Tax

When reporting mistakes persist, something subtle but devastating occurs: stakeholders lose trust in the data. Executives start making decisions based on gut feeling rather than reports. Department heads maintain shadow spreadsheets. The board questions every number presented. This trust erosion is perhaps the highest interest rate of all, because it undermines the entire purpose of business intelligence and reporting infrastructure.

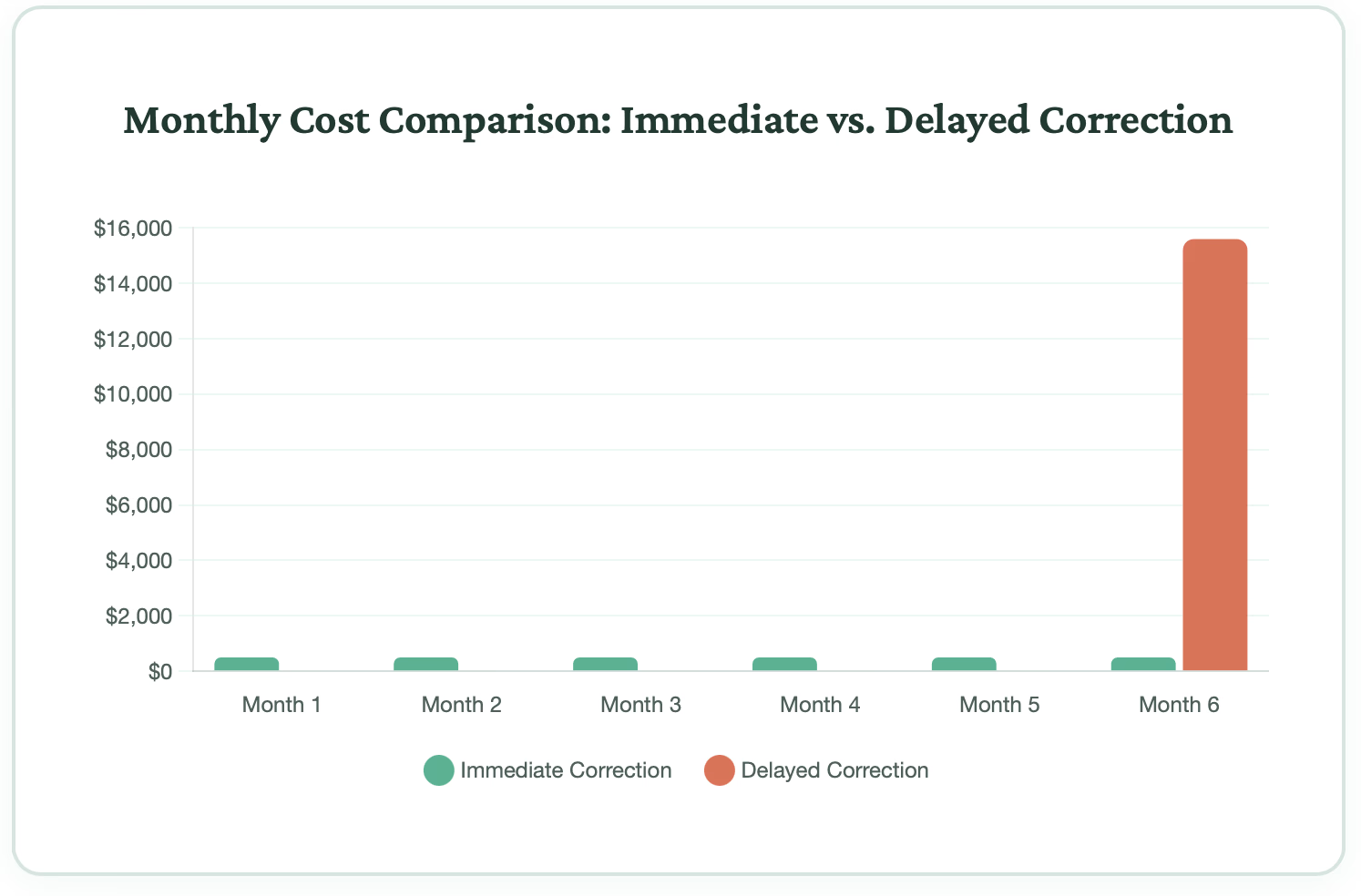

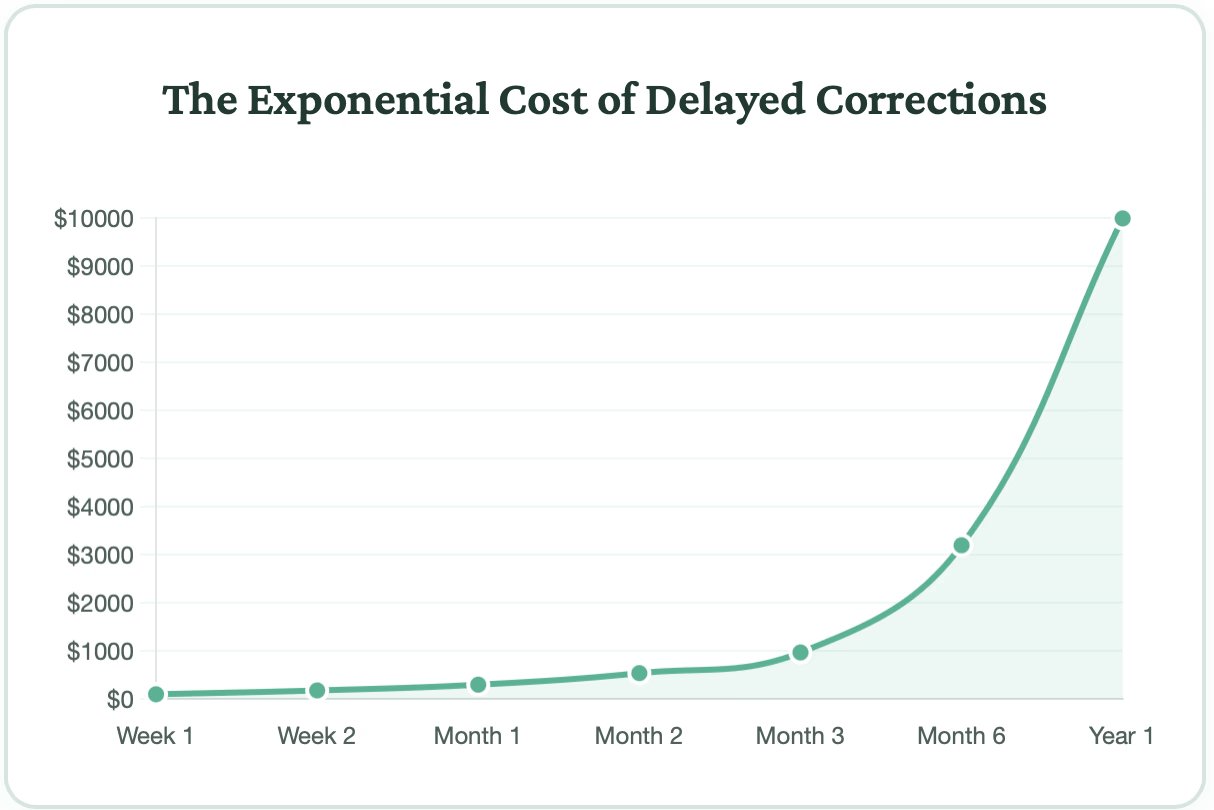

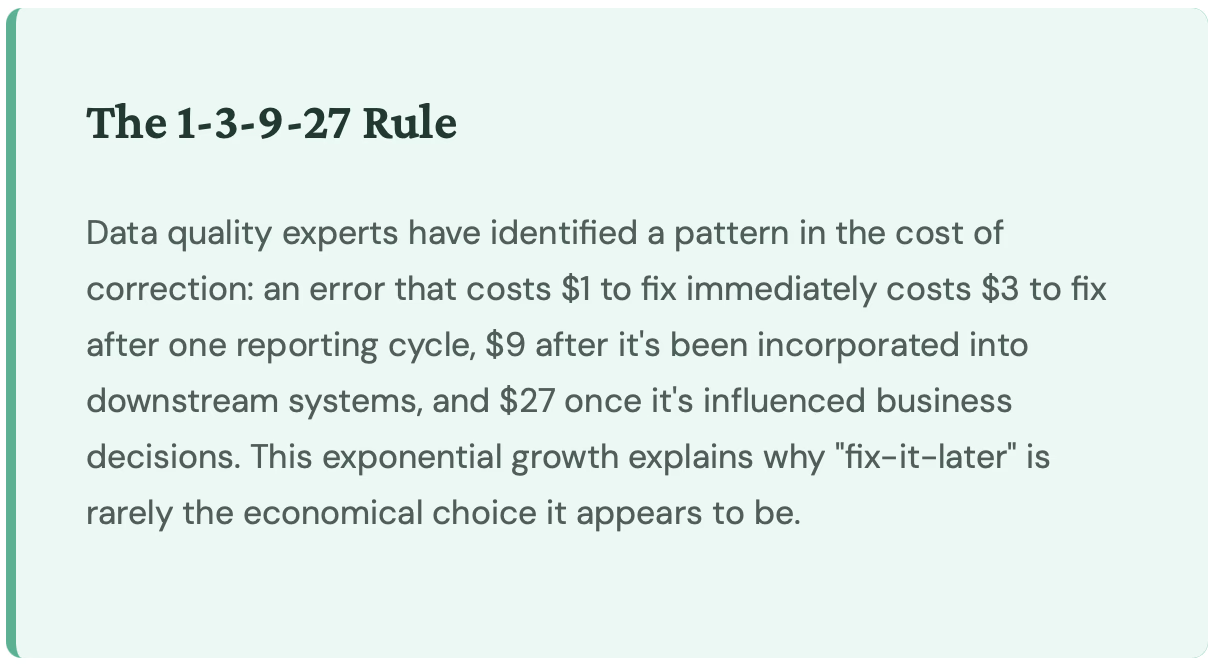

Calculating the True Cost

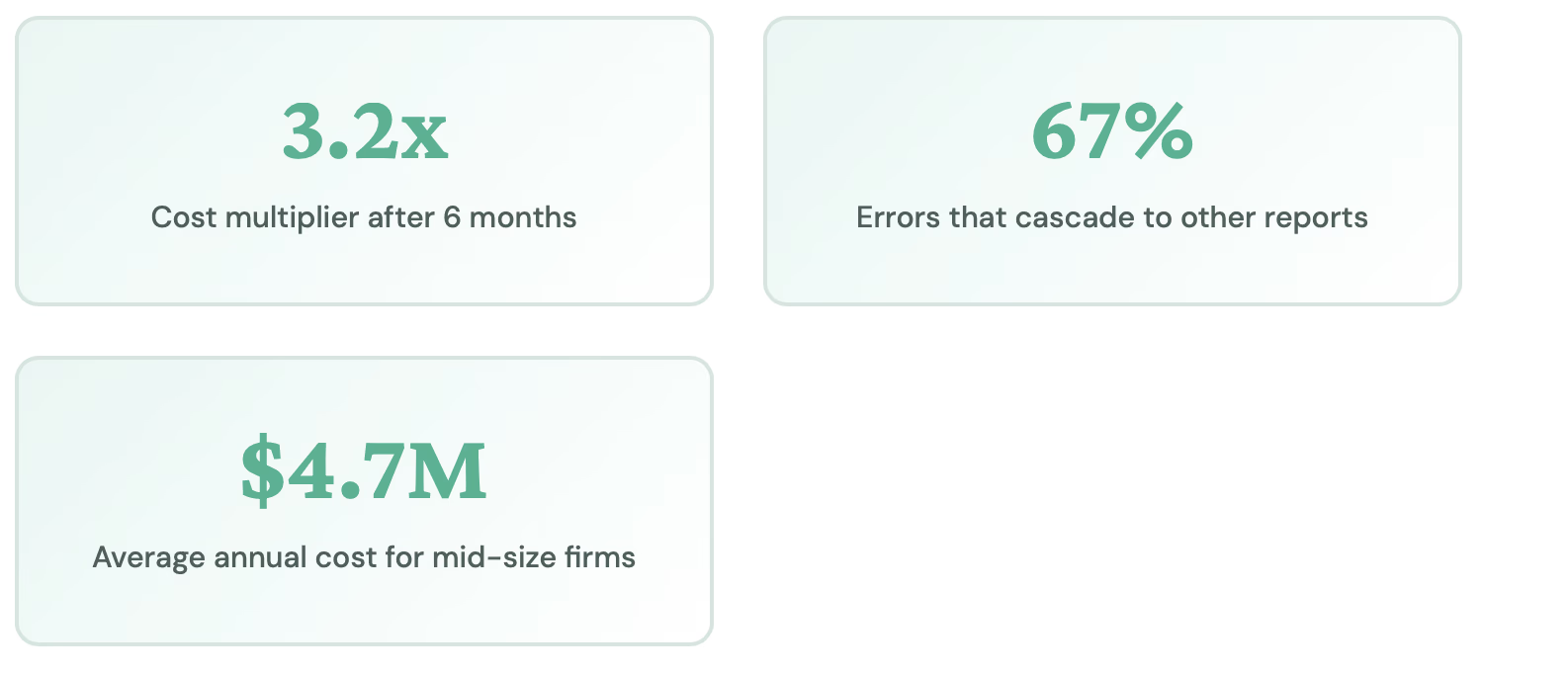

The cost of correcting a reporting error escalates dramatically with time. An immediate fix might take 30 minutes of analyst time, but waiting one month increases that to several hours of cross-report tracing and stakeholder coordination. After six months, correction may require a cross-functional team working for days. According to the PCAOB's inspection findings, auditors who identify errors late in the reporting cycle spend significantly more time on remediation than those who catch issues early through continuous monitoring (PCAOB, 2024). Research shows approximately 67% of reporting errors cascade into other reports and dashboards, creating a multiplier effect on correction costs.

Let's break down the actual dollars and hours that accumulate when reporting mistakes go unfixed. These calculations are based on industry research and interviews with finance and analytics leaders across various sectors.

Consider the staff hours alone. An immediate correction might take an analyst 30 minutes to identify, fix, and verify. Wait a month, and now you're looking at several hours to trace the error through multiple reports, coordinate corrections, and communicate changes to stakeholders. Wait six months, and you might need a cross-functional team spending days to unravel the implications and restore confidence in the corrected numbers.

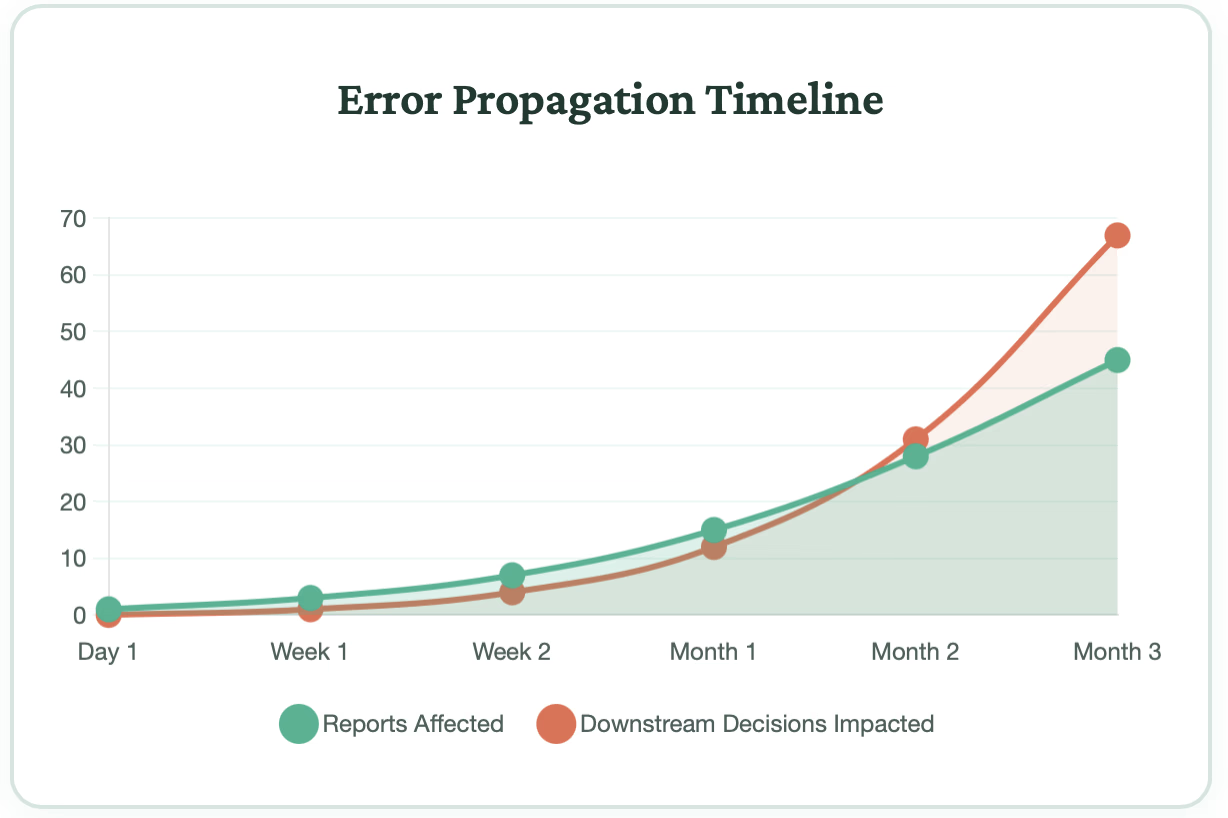

The Cascade Effect

Research shows that approximately 67% of reporting errors don't remain isolated. They cascade into other reports, dashboards, and analyses. This creates a multiplier effect where fixing the original error requires updating potentially dozens of dependent reports and recalculating metrics that were based on flawed inputs.

Breaking the Cycle

Breaking the fix-it-later cycle requires three changes: destigmatizing errors so teams report them quickly instead of hiding them, investing in automated detection systems such as data quality checks, reconciliation processes, and anomaly detection that catch errors before they reach executive reports, and establishing clear correction protocols covering triage, approval, stakeholder notification, and historical report updates to remove the friction that leads to procrastination. FASB ASC 250 (Accounting Changes and Error Corrections) provides the authoritative guidance on how reporting entities should handle and disclose corrections of errors in previously issued financial statements, underscoring the regulatory expectation that errors be addressed promptly.

The solution isn't perfection—no reporting system will ever be error-free. Instead, organizations need to shift from a "fix-it-later" to a "fix-it-fast" mentality. This requires both cultural and systematic changes.

First, organizations must destigmatize reporting errors. When mistakes carry significant political or career risk, people naturally try to hide them or downplay their significance. Creating a culture where errors are treated as valuable feedback for improving systems rather than personal failures is essential. Some of the most mature data organizations hold regular "error retrospectives" where teams analyze mistakes without blame to identify systematic improvements.

Second, invest in detection systems that catch errors early. Automated data quality checks, reconciliation processes, and anomaly detection can identify many errors before they make it into executive reports. EY's Global Financial Accounting Advisory Services reports that organizations using automated data validation tools reduce financial restatement risk by up to 45% compared to those relying on manual review alone (EY, 2024). The cost of these systems is invariably lower than the compound cost of the errors they prevent.

Third, establish clear protocols for error correction and communication. When an error is discovered, everyone should know exactly what happens next: how it gets triaged, who approves the correction, how stakeholders are notified, and how historical reports are updated. This removes the friction that often leads to procrastination.

The ROI of Swift Correction

Organizations with robust error correction processes report four measurable benefits: faster decision velocity from executives who trust their data, improved analytical productivity when analysts stop maintaining mental maps of known errors, stronger stakeholder alignment when strategy debates use trusted facts, and system simplification as addressing errors at their source reveals opportunities to streamline complex reporting architectures. PCAOB Chair Erica Williams emphasized that "getting the numbers right the first time--and correcting them quickly when errors occur--is fundamental to the integrity of financial reporting that investors depend on" (PCAOB, 2024).

Companies that have implemented robust error correction processes report measurable benefits. Beyond the obvious cost savings from avoiding compound effects, these organizations see improvements in:

Decision Velocity: Executives who trust their data make decisions faster and with greater confidence.

Analytical Productivity: When analysts aren't maintaining mental maps of known errors and workarounds, they can focus on value-adding analysis.

Stakeholder Alignment: Debates about strategy become more productive when everyone trusts they're working from the same facts.

System Simplification: Addressing errors at their source often reveals opportunities to streamline overly complex reporting architectures.