September 15, 2008. While most of Wall Street was still processing their morning coffee, Lehman Brothers filed for bankruptcy. That same day, Bank of America announced its acquisition of Merrill Lynch, and by the next day, the Federal Reserve was bailing out AIG. In the span of 72 hours, the financial world as we knew it had fundamentally changed.

But here's what many don't realize: while the headlines focused on collapsed investment banks and government bailouts, a quieter revolution was happening in the back offices of financial institutions worldwide. Regulatory reporting—once viewed as a necessary evil—suddenly became the lifeline that separated survivors from casualties.

The 2008 financial crisis wasn't just a market event; it was a stress test that exposed fatal flaws in how financial institutions tracked, reported, and understood their own risk. And the lessons learned from that chaos continue to shape how we approach regulatory compliance today.

When Standard Playbooks Fail: The 2008 Wake-Up Call

Before 2008, regulatory reporting was largely a checkbox exercise. Quarterly reports were filed on schedule, risk metrics were dutifully calculated, and everyone assumed the system was working. The problem? The crisis underscored the importance of robust risk management practices within financial institutions, as banks learned that excessive leverage and inadequate assessment of counterparty risks could lead to catastrophic outcomes.

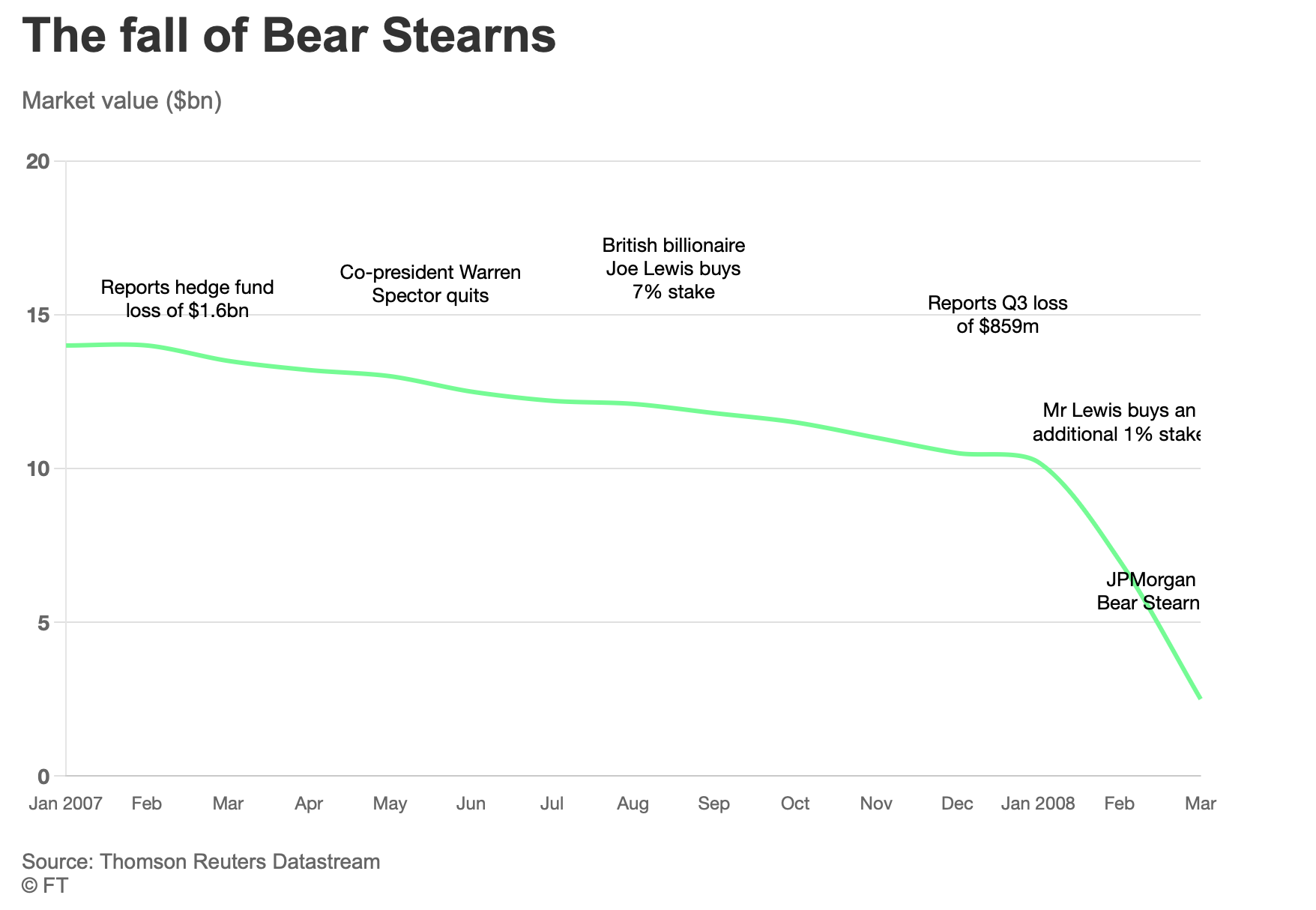

Take Bear Stearns, for example. In March 2008, the investment bank went from apparently healthy to requiring a Federal Reserve bailout in the span of days. Their regulatory filings had shown adequate capital ratios and reasonable risk exposure. Yet when the crisis hit, these reports proved woefully inadequate at capturing the firm's true financial health.

(For more information, read here)

The issue wasn't just about having the wrong numbers—it was about having the right numbers too late, in the wrong format, and without the context needed for real-time decision making.

The Reporting Revolution That Followed

The aftermath of 2008 brought unprecedented changes to regulatory reporting requirements. The Basel III capital and liquidity standards were adopted worldwide. Since the 2008 financial crisis, consumer regulators in America have more closely supervised sellers of credit cards and home mortgages in order to deter anticompetitive practices that led to the crisis.

But the changes went far beyond just new rules. The crisis fundamentally shifted how regulators and financial institutions think about reporting:

From Periodic to Real-Time: Pre-2008, quarterly reports were the gold standard. Post-crisis, regulators demanded daily, weekly, and even real-time reporting for systemically important institutions.

From Siloed to Integrated: Before the crisis, different departments often maintained separate reporting systems. The new reality demanded integrated, enterprise-wide risk reporting that could provide a holistic view of institutional health.

From Static to Dynamic: Traditional reports were snapshots in time. Modern regulatory reporting requires dynamic modeling that can stress-test scenarios and project forward-looking risks.

Lessons from the European Sovereign Debt Crisis (2010-2012)

Just as the financial world was beginning to implement lessons from 2008, Europe faced its own crisis. The European sovereign debt crisis that began in 2010 provided another masterclass in the critical importance of accurate, timely regulatory reporting.

Greece's debt crisis wasn't just about unsustainable borrowing—it was also about reporting inconsistencies that masked the true scope of the problem. When accurate data finally emerged, it revealed that Greece's budget deficit was actually double what had been previously reported to the European Union.

This crisis led to the implementation of enhanced European regulatory frameworks, including more stringent reporting requirements under COREP (Common Reporting) and FINREP (Financial Reporting) standards. European banks learned that transparency isn't just about compliance—it's about survival.

The COVID-19 Stress Test: Digital Reporting Under Pressure

Fast forward to March 2020. As the world went into lockdown, financial markets experienced volatility not seen since 2008. But this time, something was different. While markets crashed and economies shuttered, regulatory reporting systems largely held firm.

The difference? Nearly a decade of post-crisis investments in digital infrastructure, automated reporting systems, and real-time risk monitoring. Banks that had modernized their regulatory reporting capabilities found themselves able to maintain operations even with remote workforces and unprecedented market conditions.

Those still relying on manual processes and legacy systems faced a different reality. Suddenly, the quarterly reporting cycles that used to take weeks of coordinated effort had to be completed by teams working from kitchen tables, using VPNs to access critical systems.

The Modern Regulatory Reporting Playbook

Today's most resilient financial institutions have learned to treat regulatory reporting not as a compliance burden, but as a strategic capability. Here's what separates the leaders from the laggards:

Automation is Non-Negotiable: Manual data collection and report preparation are vestiges of a pre-digital age. Modern regulatory reporting leverages AI and machine learning to automate data collection, validation, and report generation.

Data Quality is Everything: The old garbage-in, garbage-out principle has never been more relevant. Leading institutions invest heavily in data governance, implementing controls that catch errors before they propagate through reporting systems.

Integration Across Systems: Rather than maintaining separate reporting silos, smart organizations build integrated platforms that can serve multiple regulatory requirements while providing real-time visibility into institutional risk.

Scenario Planning and Stress Testing: Static reporting tells you where you've been. Dynamic modeling tells you where you're going. Modern regulatory reporting includes robust stress testing capabilities that can model various crisis scenarios.

The Technology Edge: Why AI Matters More Than Ever

The rise of artificial intelligence in regulatory reporting isn't just about efficiency—it's about survival in an increasingly complex regulatory landscape. Consider the volume challenge: a major bank might need to file hundreds of different regulatory reports across multiple jurisdictions, each with different formats, timing requirements, and data specifications.

Traditional approaches simply don't scale. But AI-powered systems can:

- Automatically map data across different regulatory frameworks

- Identify anomalies that might indicate data quality issues or emerging risks

- Generate narrative explanations for regulatory submissions

- Continuously monitor regulatory changes and update reporting processes accordingly

This isn't theoretical—it's happening now. Financial institutions that have embraced AI for regulatory reporting report dramatic improvements in accuracy, timeliness, and cost efficiency.

Looking Forward: Preparing for the Next Crisis

History teaches us that financial crises are not one-time events—they're recurring features of modern financial systems. The question isn't whether there will be another crisis, but when, and whether your organization will be prepared.

The institutions that will thrive in the next crisis share several characteristics:

Real-Time Visibility: They can generate comprehensive risk reports not just quarterly or monthly, but daily or even hourly when conditions warrant.

Regulatory Agility: Their systems can quickly adapt to new reporting requirements without requiring months of development work.

Data-Driven Decision Making: They use regulatory data not just for compliance, but as a strategic asset for risk management and business decision-making.

Technology Integration: They've moved beyond viewing technology as a cost center, instead treating it as a strategic capability that enables competitive advantage.

The Human Element: Technology Enablement, Not Replacement

While technology plays an increasingly important role in regulatory reporting, the human element remains crucial. The most successful organizations combine technological capability with deep regulatory expertise and business judgment.

AI can process vast amounts of data and generate reports at superhuman speed, but it takes human insight to understand what the data means, identify emerging risks, and communicate effectively with regulators. The future belongs to organizations that can seamlessly blend technological capability with human expertise.

Conclusion: Crisis as Catalyst

Every major financial crisis has served as a catalyst for regulatory reporting evolution. The 2008 financial crisis taught us about the importance of comprehensive risk reporting. The European sovereign debt crisis emphasized the need for transparency and consistency. The COVID-19 pandemic proved the value of digital infrastructure and remote capabilities.

As we look toward an uncertain future—with emerging risks from cryptocurrency, climate change, and geopolitical instability—one thing is clear: regulatory reporting will continue to evolve. The institutions that view this evolution as an opportunity rather than a burden will be the ones that not only survive the next crisis but also emerge stronger.

The technology exists. The lessons have been learned. The question is: will your organization be ready when the next test comes?

The next time markets go haywire, will your team be scrambling to meet deadlines while hoping for the best? Or will you be watching AI-powered systems flawlessly execute your regulatory reporting while you focus on steering the ship through the storm?

This analysis draws from extensive research into regulatory reporting evolution following major financial crises, including insights from post-2008 regulatory reforms, European banking supervision enhancements, and recent developments in AI-powered compliance technology.