The Traditional Mindset: More is Better

The conventional approach to audit risk management assumes that increasing the frequency of inspections proportionally reduces risk. However, evidence from organizations worldwide shows that inspection volume does not correlate strongly with risk reduction. The PCAOB's annual inspection reports consistently show that audit deficiency rates are not simply a function of the number of inspections performed, but rather reflect the quality and depth of audit procedures applied (PCAOB, 2024). The effectiveness of an audit program depends on how well inspections are designed and targeted, not how many are conducted.

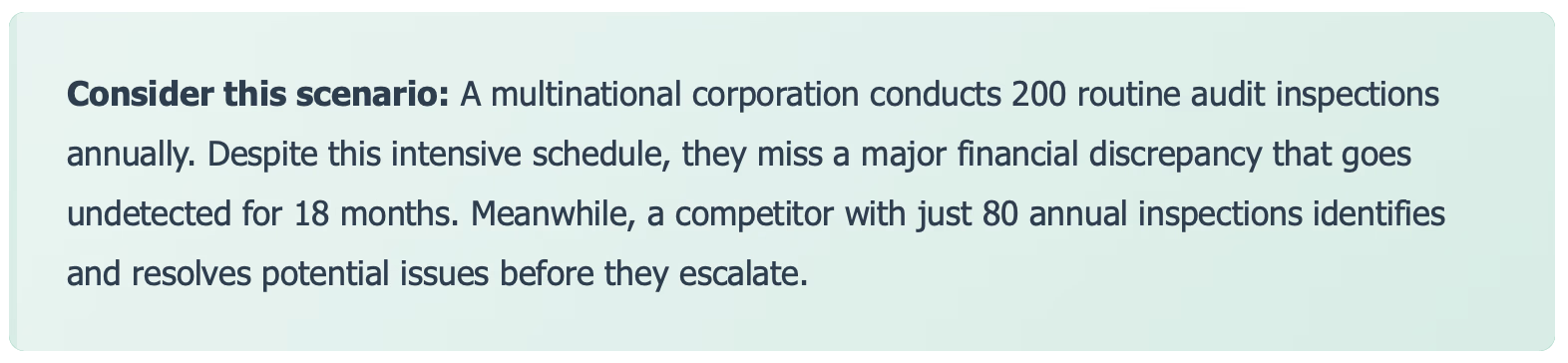

For decades, finance teams have operated under a simple assumption: the more audit inspections you conduct, the safer your organization. It's an intuitive belief. After all, wouldn't checking everything multiple times catch every possible error or fraud?

But here's the uncomfortable truth that's emerging from organizations worldwide: inspection frequency doesn't correlate with risk reduction as strongly as we once believed.

What's the difference? The answer lies not in how many inspections are performed, but in how well they're designed and executed.

Why More Inspections Can Actually Increase Risk

Excessive audit inspections introduce three specific vulnerabilities: inspection fatigue where teams reduce thoroughness and treat audits as checkbox exercises, resource dilution where hours spent on routine checks displace strategic risk analysis and investigation of genuine red flags, and an illusion of coverage where frequent but shallow inspections create false confidence in comprehensive oversight. PCAOB Chair Erica Williams noted in a 2023 address that "audit quality is not measured by volume of procedures performed, but by the effectiveness of those procedures in identifying material misstatements" (PCAOB, 2023). Some organizations have improved detection rates by reducing inspection volume and redirecting resources to data analytics and targeted deep dives.

It sounds counterintuitive, but an overabundance of inspections can create a false sense of security while introducing new vulnerabilities:

1. Inspection Fatigue

When your team is constantly being audited, something dangerous happens: they start going through the motions. The thoroughness that makes inspections valuable erodes into checkbox exercises. A Deloitte audit quality report found that audit teams handling excessive workloads were significantly more likely to miss material misstatements compared to teams with manageable caseloads (Deloitte, 2023). Auditors become desensitized, and the finance team becomes skilled at "performing" compliance rather than embodying it.

2. Resource Dilution

Every hour spent on a routine inspection is an hour not spent on strategic risk analysis, process improvement, or investigating genuine red flags. Organizations can become so busy inspecting that they lose sight of what they're inspecting for.

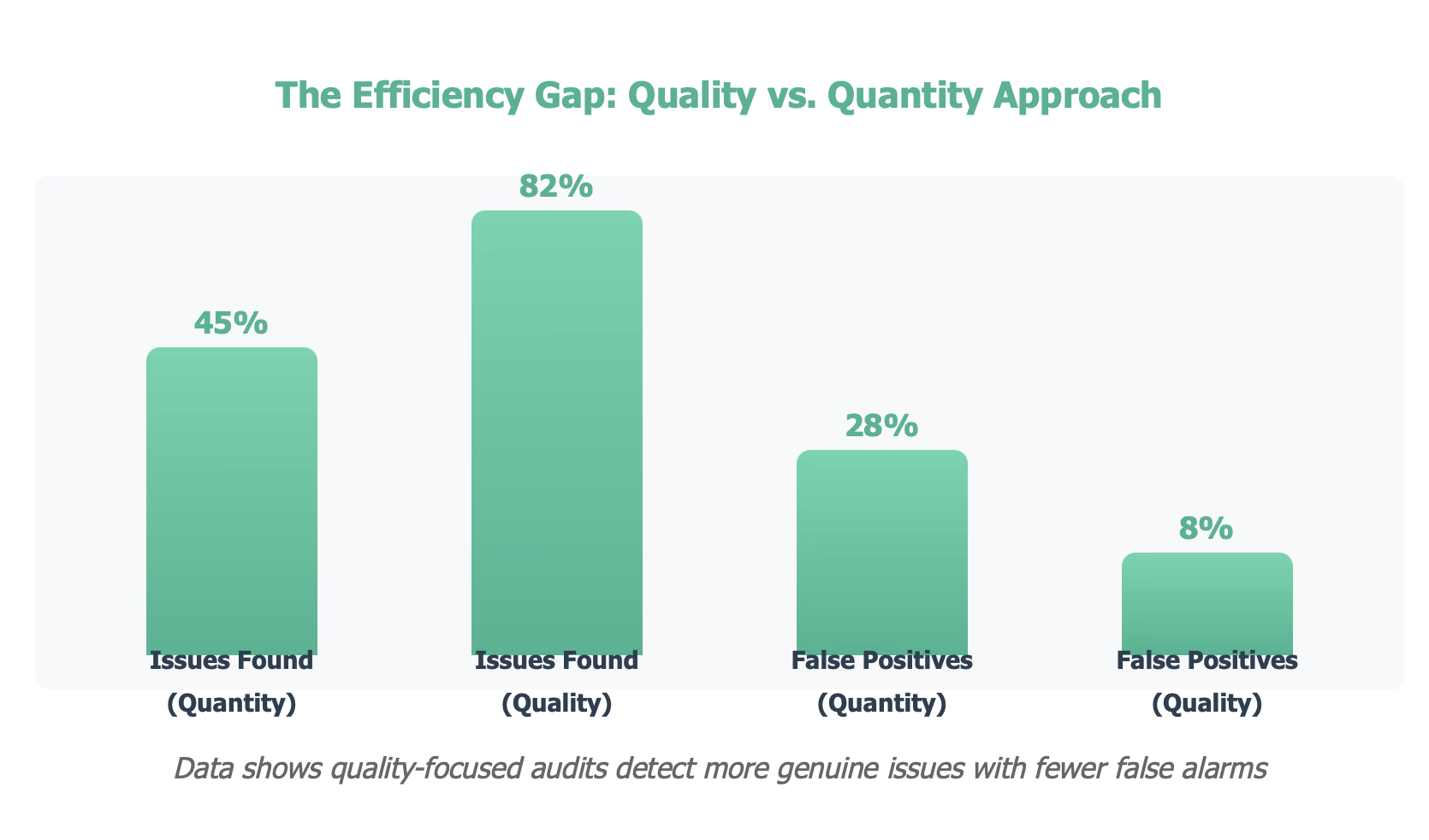

Real-world impact: A Fortune 500 company reduced their audit inspections by 40% while increasing their detection rate of material misstatements by 35%. How? They redirected resources toward data analytics, risk-based sampling, and specialized deep-dive audits in high-risk areas.

3. The Illusion of Coverage

Multiple shallow inspections create an illusion of comprehensive coverage. Organizations believe they're protected because "we audit that department every quarter," but if those audits are superficial, the protection is illusory.

The Quality Revolution: A New Audit Philosophy

The shift from audit volume to audit intelligence centers on three practices: risk-based prioritization that concentrates resources on the highest-risk areas identified through data analytics and historical trends, deeper substantive testing that examines whether controls would withstand real-world stress rather than simply verifying documentation exists, and continuous automated monitoring that flags anomalies in real time so human auditors can focus on complex investigation. The Institute of Internal Auditors (IIA) has endorsed risk-based auditing as a core professional standard, emphasizing that internal audit resources should be allocated proportional to risk rather than spread uniformly (IIA, 2024).

Progressive finance teams are embracing a paradigm shift: from audit volume to audit intelligence. Here's what this transformation looks like:

Risk-Based Prioritization

Instead of spreading resources evenly, quality-focused audits concentrate on areas where risks are highest. This means:

- Data analytics identify patterns and anomalies that warrant investigation

- Historical trends inform where problems are most likely to emerge

- **Business intelligence **highlights departments or processes undergoing significant change

- External factors like regulatory changes or market volatility guide audit focus

Deeper, Not Broader

Quality audits go beneath the surface. Rather than checking if documentation exists, they examine whether processes are genuinely robust. Rather than verifying that controls are in place, they test whether those controls would withstand real-world stress.

Continuous Monitoring vs. Periodic Checking

Technology has enabled a shift from periodic inspections to continuous monitoring. Automated systems can flag anomalies in real-time, allowing human auditors to focus their expertise where it's most needed rather than on routine verification tasks. According to KPMG's audit innovation report, firms that adopted continuous monitoring and data analytics detected anomalies 40-60% faster than those relying solely on periodic manual inspections (KPMG, 2024).

Implementing a Quality-First Audit Strategy

A quality-first audit strategy requires four steps: conducting a comprehensive risk assessment to map genuine vulnerabilities, investing in data analytics and AI-powered anomaly detection for continuous monitoring, upskilling the audit team in forensic analysis and data interpretation rather than checklist verification, and redefining success metrics to track issues prevented, detection-to-resolution time, and risk prediction accuracy instead of inspection count. The AICPA's Audit Quality Center recommends that firms measure audit effectiveness through outcome-based metrics rather than activity-based counts (AICPA, 2024).

Transitioning from quantity to quality requires both cultural and operational changes:

Step 1: Conduct a Risk Assessment

Map your organization's genuine risk landscape. Where are the vulnerabilities? What processes have the highest potential for material impact if they fail? This becomes your audit roadmap.

Step 2: Invest in Technology

Data analytics, AI-powered anomaly detection, and automated monitoring tools allow you to maintain oversight without constant manual inspection. These systems work 24/7, flagging issues that require human expertise.

Step 3: Upskill Your Team

Quality audits require different skills than quantity audits. Your team needs training in forensic analysis, data interpretation, and complex problem-solving rather than just checklist verification.

Step 4: Redefine Success Metrics

Stop measuring audit effectiveness by number of inspections completed. Instead, track:

- Issues identified and prevented before they become problems

- Time from issue detection to resolution

- Accuracy rate of risk predictions

- Stakeholder satisfaction with audit insights

- Return on investment for audit resources

The Bottom Line

SEC Chief Accountant Paul Munter has stated that "audit committees should focus on ensuring their auditors are applying professional skepticism and appropriate rigor, rather than simply tracking the number of procedures performed" (SEC Office of the Chief Accountant, 2023). The evidence across organizations that have shifted to quality-focused audit programs shows that fewer, well-targeted inspections deliver stronger risk management outcomes than high-volume routine checks.

This approach does not mean reducing oversight. It means applying oversight strategically: using technology for continuous monitoring, directing human expertise to high-risk areas, and designing audits that test whether controls withstand real-world stress rather than simply verifying documentation exists.